Alberta is undergoing a profound demographic and economic transformation. As hundreds of thousands of new residents flock to the province, drawn by affordable housing and robust employment opportunities, the foundational pillars of provincial infrastructure are being tested. Chief among these is the public healthcare system. Alberta Health Services (AHS), historically one of the most comprehensive integrated health systems in Canada, is facing unprecedented strain. Wait times for family physicians, specialized diagnostics, and elective procedures have reached historic highs.

Yet, where public infrastructure faces bottlenecks, Alberta’s deeply ingrained entrepreneurial spirit finds opportunity. A parallel healthcare market is experiencing a quiet but massive explosion across the province. From membership-based concierge medical practices in downtown Calgary to independent Nurse Practitioner-led clinics in rural Alberta, and specialized diagnostic centers catering to the industrial workforce, the business of private care is booming.

This comprehensive guide is designed for potential residents trying to understand their healthcare options, investors looking at commercial real estate and healthcare ventures, business owners navigating the regulatory landscape, and technical professionals analyzing the systemic shift in service delivery. We will break down the mechanics of this parallel market, explore the underlying business models, and analyze exactly what this shift costs the average Albertan.

The following economic facts are based on current Alberta provincial data and market trends.

1. The Historical and Macroeconomic Context

To understand the current boom in private health clinics, one must first understand the macroeconomic forces and historical context that have shaped Alberta’s healthcare landscape.

The Canada Health Act vs. Provincial Innovation

Healthcare in Canada is publicly funded but provincially administered. The Canada Health Act (CHA) mandates that all “medically necessary” services provided by hospitals and physicians must be covered by the public purse, free at the point of care. However, the CHA leaves significant room for interpretation regarding what constitutes “medically necessary,” and it does not explicitly prohibit the private delivery of care, provided that the care is publicly funded.

Alberta has a long history of pushing the boundaries of the CHA to introduce market efficiencies. From the privatization of laboratory services to the contracting out of specific surgical procedures (such as cataracts and orthopedic surgeries) to independent Non-Hospital Surgical Facilities (NHSFs), Alberta has frequently utilized private enterprise to clear public backlogs.

The Demographic Catalyst

The current explosion in private clinics is largely driven by a demographic catalyst. In recent years, Alberta has led the country in interprovincial migration, absorbing populations equivalent to small cities in a matter of months.

- Population Growth: Alberta’s population growth rate has recently hovered around 4% annually, a staggering figure that places immense pressure on existing public services.

- Physician Shortages: A combination of pandemic burnout, shifting provincial funding models, and an aging physician workforce has led to a critical shortage of primary care providers. Hundreds of thousands of Albertans currently do not have a regular family doctor.

- The Aging Population: The baby boomer generation is entering its highest healthcare-utilization years, requiring more complex, continuous, and specialized care.

These three factors have created a massive gap between the supply of public healthcare and the demand from citizens. Nature abhors a vacuum, and the free market has stepped in to fill it.

2. The Mechanics of the Parallel Market

How do private clinics operate legally in a country known for universal public healthcare? The answer lies in the careful navigation of regulatory frameworks, a focus on uninsured services, and the utilization of alternative healthcare professionals.

The “Uninsured Services” Framework

Private clinics in Alberta generally operate by offering services that are not deemed medically necessary under the provincial health insurance plan (Alberta Health Care Insurance Plan – AHCIP).

- Preventative and Proactive Care: AHCIP covers you when you are sick. It generally does not cover comprehensive, proactive longevity planning, advanced genetic screening, or holistic nutritional counseling.

- Third-Party Payers: Many private clinics focus on services paid for by third parties, such as the Workers’ Compensation Board (WCB), the Royal Canadian Mounted Police (RCMP), or corporate employers who require independent medical evaluations for their staff.

The Rise of Nurse Practitioner (NP) Clinics

One of the most significant recent shifts in Alberta’s healthcare economy is the empowerment of Nurse Practitioners. NPs are highly trained registered nurses with advanced university education who can diagnose illnesses, order and interpret tests, prescribe medications, and perform medical procedures.

Historically, NPs were salaried employees of AHS or worked under physicians. However, recent provincial policy changes have allowed NPs to operate independently and bill the government directly for their services.

- The Economic Impact: This has opened the floodgates for NP-led clinics. Because NPs can operate with lower overhead than traditional physician-led clinics and can now access direct public funding for primary care, they represent a highly viable business model. Furthermore, many NP clinics supplement their public billing with private, out-of-pocket wellness services, creating a robust hybrid revenue model.

The “Opted-Out” Physician

While rare, physicians in Alberta can legally “opt out” of the public system. If a doctor opts out, they cannot bill AHCIP for any services. Instead, they bill the patient directly at a market rate. The patient cannot submit this bill to the government for reimbursement. These opted-out physicians often form the backbone of elite concierge medical practices, catering to high-net-worth individuals and corporate executives.

3. Deep Dive: Emerging Business Models in Private Care

The private healthcare sector in Alberta is not monolithic. It is segmented into several distinct business models, each with its own capital requirements, target demographics, and revenue streams.

Model A: Membership-Based Concierge Medicine

Concierge medicine (also known as boutique medicine) is designed to offer highly personalized, unhurried care in exchange for an annual retainer or membership fee.

- The Value Proposition: Patients are paying for access and time. Instead of waiting weeks for a 10-minute appointment, members get same-day or next-day access, 24/7 telemedicine contact with their provider, and appointments that last 45 to 60 minutes.

- The Target Demographic: High-net-worth individuals, busy professionals, and corporations purchasing executive health packages as a retention perk.

- The Revenue Model:

- Annual membership fees ranging from $2,500 to $6,000+ per adult.

- Corporate retainers.

- Ancillary billing for specialized, non-insured treatments (e.g., advanced cardiac screening).

- Economic Reality: A traditional family doctor might need a roster of 1,500 to 2,000 patients to remain profitable under the public fee-for-service model. A concierge physician can cap their roster at 300 to 500 patients, generating equal or greater revenue while dramatically reducing burnout and administrative overhead.

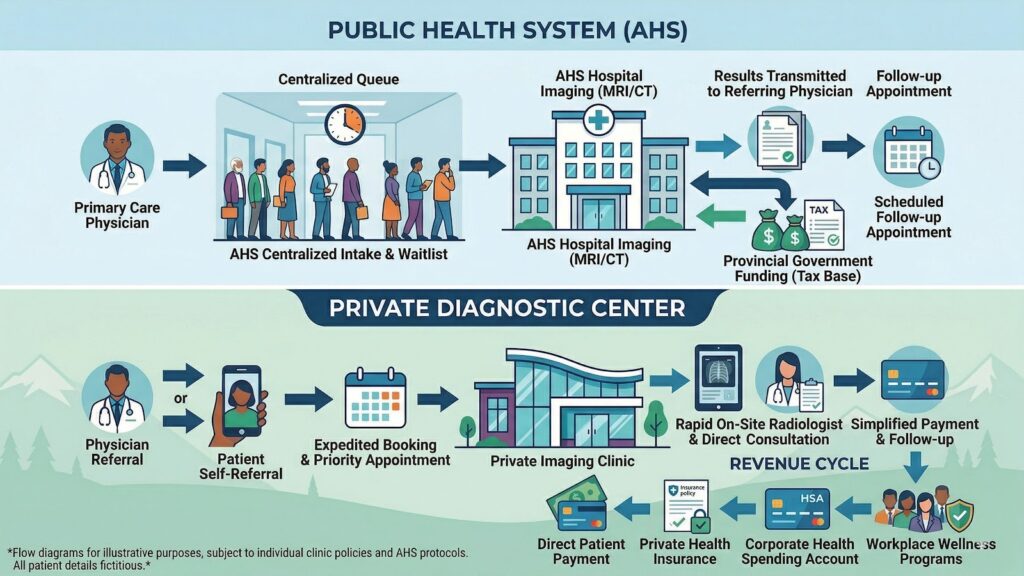

Model B: Specialized Diagnostic Centers

For many Albertans, the bottleneck in the healthcare system is not seeing a general practitioner, but getting a specialized scan to diagnose an injury. Wait times for public MRIs and CT scans can stretch from several months to over a year for non-urgent cases.

- The Value Proposition: Speed. For a tradesperson, oilfield worker, or independent contractor, waiting eight months for an MRI on a torn meniscus means eight months of lost income. Paying out-of-pocket to get scanned tomorrow is a simple return-on-investment calculation.

- The Target Demographic: Injured workers, athletes, and individuals suffering from chronic pain who need immediate diagnostic clarity.

- The Revenue Model:

- Direct out-of-pocket payments (e.g., $700 to $1,200 for a private MRI).

- Contracts with WCB and professional sports teams.

- Corporate health accounts.

- Capital Expenditure (CapEx): This is the most capital-intensive model. Siting, purchasing, and installing an MRI machine, alongside the necessary lead-lining and specialized HVAC systems, requires millions of dollars in upfront capital.

Model C: Holistic Wellness, Longevity, and MedSpas

This is the fastest-growing segment of the private health market. These clinics blur the line between traditional medicine, preventative health, and aesthetic improvement.

- The Value Proposition: Optimization rather than just disease management. These clinics focus on “healthspan” (the portion of life spent in good health) rather than just lifespan.

- Services Offered: Intravenous (IV) vitamin therapy, bio-identical hormone replacement therapy (BHRT), medical weight loss programs (such as GLP-1 agonists), functional medicine diagnostics, and medical aesthetics (Botox, dermal fillers).

- The Target Demographic: A broad spectrum of middle-to-upper-class Albertans, skewing heavily toward demographics aged 35-60 who are willing to invest disposable income into anti-aging and wellness.

- The Revenue Model: High-margin, fee-for-service transactions. Because these services are entirely outside the CHA, pricing is dictated purely by market demand. Margins on services like IV therapy and medical aesthetics can range from 40% to 70%.

4. The Economics for Investors and Business Owners

For entrepreneurs, commercial real estate investors, and clinical professionals looking to enter the Alberta market, the private health sector offers compelling opportunities, but it requires navigating complex operational economics.

Analyzing Capital Expenditures (CapEx)

Building a modern health or wellness clinic is significantly more expensive than standard office space due to stringent health and safety regulations, specialized plumbing, and privacy requirements.

- Leasehold Improvements: In major centers like Calgary or Edmonton, outfitting a base-building commercial space into a medical clinic can cost between $150 and $300 per square foot. This includes soundproofing (essential for patient privacy), specialized millwork, medical-grade flooring, and upgraded HVAC systems to manage air exchanges.

- Equipment Costs: While a basic family practice requires minimal equipment, a functional medicine or longevity clinic requires substantial investment in EKG machines, body composition analyzers (DEXA scanners), compounding equipment, and specialized refrigeration for biologics.

- Technology Stack: Modern private clinics compete on user experience. This requires robust, secure Electronic Medical Record (EMR) systems integrated with patient-facing apps for booking, telemedicine, and lab result tracking.

Managing Operational Expenditures (OpEx)

The primary challenge for any healthcare business in Alberta today is staffing. Private clinics are in direct competition with AHS for talent.

- The War for Talent: To attract top-tier Registered Nurses (RNs), Licensed Practical Nurses (LPNs), and medical office assistants, private clinics must offer competitive compensation packages. While AHS offers strong pensions and union benefits, private clinics often counter with better working hours (no night shifts), lower patient-to-staff ratios, and profit-sharing models.

- Estimated Staffing Costs:

- Nurse Practitioners: $120,000 – $160,000+ base salary or revenue-sharing split.

- Registered Nurses: $85,000 – $110,000.

- Clinic Managers: $70,000 – $95,000.

- Insurance and Liability: Malpractice insurance, commercial general liability, and specialized cyber-security insurance (due to the handling of sensitive patient data) constitute a significant portion of fixed monthly OpEx.

Commercial Real Estate Impact

The boom in private clinics is a major driver of commercial real estate absorption in Alberta. Retail landlords are increasingly courting medical tenants because they are “sticky”—once a clinic invests heavily in leasehold improvements, they rarely move. Furthermore, medical clinics drive consistent, high-quality foot traffic to retail plazas, benefiting adjacent businesses like pharmacies, cafes, and fitness centers.

5. What It Costs the Average Albertan

The shift toward a parallel healthcare market fundamentally alters the financial landscape for the average Alberta family. While public care remains free at the point of delivery, the hidden costs of waiting—lost wages, prolonged pain, deteriorating health—are pushing middle-class Albertans to open their wallets.

Breaking Down the Out-of-Pocket Expenses

To understand the financial burden, we must look at the typical costs associated with the private market:

1.Primary Care/Concierge Access:

- Cost: $2,500 to $4,000 per year, per adult.

- Impact: For a family of four, securing guaranteed, immediate access to a physician can cost upwards of $10,000 annually. This is generally paid post-tax, making it a significant household expense.

2.Private Diagnostics:

- Cost: $750 for a single-site MRI; up to $2,500 for a comprehensive preventative full-body scan.

- Impact: Often treated as a one-off emergency expense. Many Albertans dip into savings or use credit cards to bypass public waitlists for orthopedic injuries.

3.Wellness and Optimization:

- Cost: $150 to $250 per IV therapy session; $300 to $500 for initial functional medicine consultations; $300+ per month for medical weight loss prescriptions.

- Impact: Treated as a recurring lifestyle and wellness expense, often replacing discretionary spending on personal training or luxury goods.

The Role of Private Health Insurance and HSAs

The average Albertan rarely pays for these services entirely out of their own pocket. The corporate benefits landscape has evolved rapidly to accommodate the private health boom.

- Health Spending Accounts (HSAs): Unlike traditional health insurance, which dictates exactly what services are covered (e.g., $500 for massage therapy), an HSA provides a lump sum of tax-free money (e.g., $2,000 per year) that the employee can spend on any eligible medical expense recognized by the Canada Revenue Agency (CRA). Many Albertans use their employer-provided HSAs to fund private diagnostic scans or specialized NP consultations.

- Executive Health Benefits: To attract top talent in Alberta’s highly competitive energy, tech, and engineering sectors, corporations are increasingly purchasing corporate memberships at concierge clinics for their executive teams. This ensures their key personnel are never stuck on a waitlist, minimizing corporate downtime.

The Equity Equation

The educational reality of this economic shift is the entrenchment of a two-tiered system. Albertans with high disposable income or excellent corporate benefits can access immediate, preventative, and highly personalized care. Those relying solely on the public system face a system geared toward acute crisis management and long wait times. This economic bifurcation is a critical factor for new residents and policymakers to understand.

6. Regulatory Frameworks and Long-Term Growth Outlook

The future of Alberta’s private health and wellness clinics depends heavily on the intersection of market demand and provincial regulatory policy.

Government Policy Shifts

The current provincial government has shown a strong willingness to integrate private delivery into the public system to reduce wait times. The restructuring of Alberta Health Services into specialized provincial agencies (focusing on primary care, acute care, continuing care, and mental health) signals a move toward a more decentralized, competitive model.

Furthermore, the government’s commitment to funding independent Nurse Practitioner clinics is a watershed moment. It proves that the province is willing to fund the service rather than dictating that the service must be delivered by a physician within a traditional AHS facility.

Future Projections for the Industry

The economic indicators point toward sustained, aggressive growth in the private health sector over the next decade.

1.Consolidation: The current market is highly fragmented, consisting mostly of independent, physician-owned or NP-owned clinics. Over the next five to ten years, expect to see private equity firms and large corporate health entities begin rolling up these independent clinics into massive provincial networks to achieve economies of scale.

2.Technological Integration: The most successful private clinics will be those that seamlessly integrate AI-driven diagnostics, continuous wearable health monitoring (like continuous glucose monitors and smart rings), and telemedicine. The clinic of the future will be a data-management hub as much as a physical treatment center.

3.Expansion of Scope: As the public system continues to focus its resources on acute and emergency care, the private sector will absorb almost all preventative, longevity, and minor-acute care. We will likely see private urgent care clinics (charging a facility fee or membership) become commonplace in major suburban centers.

Conclusion: A Permanent Shift in the Alberta Economy

The boom in private health and wellness clinics in Alberta is not a temporary trend; it is a permanent structural shift in the provincial economy. Driven by explosive population growth, shifting demographics, and an entrepreneurial culture that favors market-based solutions, the business of care has become one of Alberta’s most dynamic economic sectors.

For the average Albertan, navigating this new landscape requires financial planning and a clear understanding of how to leverage employer benefits and Health Spending Accounts. For investors, engineers, and business owners, the healthcare sector represents a frontier of massive opportunity—provided one can navigate the complex regulatory environment, secure top-tier clinical talent, and deliver a standard of care that justifies the out-of-pocket cost. Alberta is no longer just the energy capital of Canada; it is rapidly becoming the nation’s laboratory for healthcare innovation and private market integration.

Sources and References

- Alberta Health Services (AHS): Publicly available data on wait times for diagnostic imaging and surgical procedures.

- Government of Alberta: Ministry of Health policy announcements regarding Nurse Practitioner funding models and the restructuring of provincial health agencies.

- Statistics Canada: Interprovincial migration reports and demographic aging projections for the Province of Alberta.

- Canada Health Act: Federal legislative framework regarding medically necessary services.

- Commercial Real Estate Market Reports: Industry data (CBRE, Colliers) on medical office space absorption and leasehold improvement costs in Calgary and Edmonton.