For over a century, the word “drilling” in Alberta has been synonymous with one thing: hydrocarbons. From the historic gusher at Leduc No. 1 to the massive oil sands operations in Fort McMurray, the province’s economic identity has been forged in oil and gas. However, a quiet revolution is bubbling beneath the surface—literally. As the global demand for electric vehicles (EVs) and grid-scale energy storage skyrockets, Alberta is discovering that its greatest legacy—the vast, deep-well infrastructure of the Western Canadian Sedimentary Basin (WCSB)—might be the key to unlocking a different kind of liquid gold.

This is the story of Alberta’s “Petro-lithium” sector, a burgeoning industry that seeks to transform the province into a global powerhouse for battery-grade lithium. By leveraging existing oilfield technology, geological data, and a highly skilled workforce, Alberta is positioning itself to bypass the traditional, environmentally taxing methods of lithium extraction used in South America and Australia.

The following economic facts are based on current Alberta provincial data and market trends.

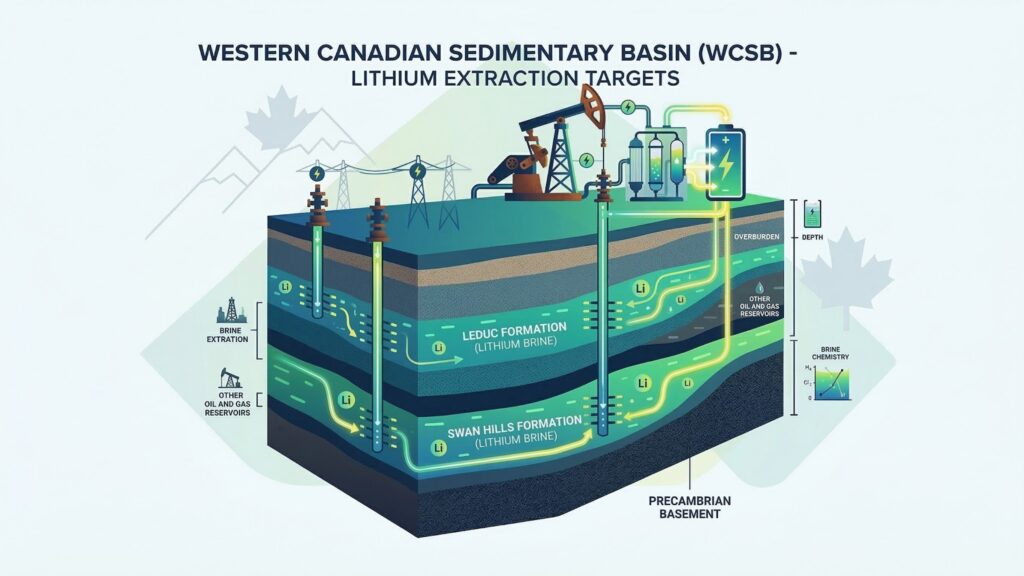

1. The Geological Treasure Map: Why Alberta?

To understand the potential of lithium in Alberta, one must look back hundreds of millions of years. During the Devonian period, much of what is now Western Canada was covered by an ancient inland sea. As organic matter settled and geological shifts occurred, massive carbonate reefs and sandstone reservoirs were formed. While these formations trapped the oil and gas that built Alberta, they also trapped enormous quantities of formation water—hypersaline brines.

The Leduc and Swan Hills Formations

The primary targets for lithium extraction are the Leduc and Swan Hills formations. For decades, these reservoirs have produced vast quantities of water as a byproduct of oil and gas extraction. Historically, this “produced water” was seen as a nuisance—a waste product to be reinjected into the ground.

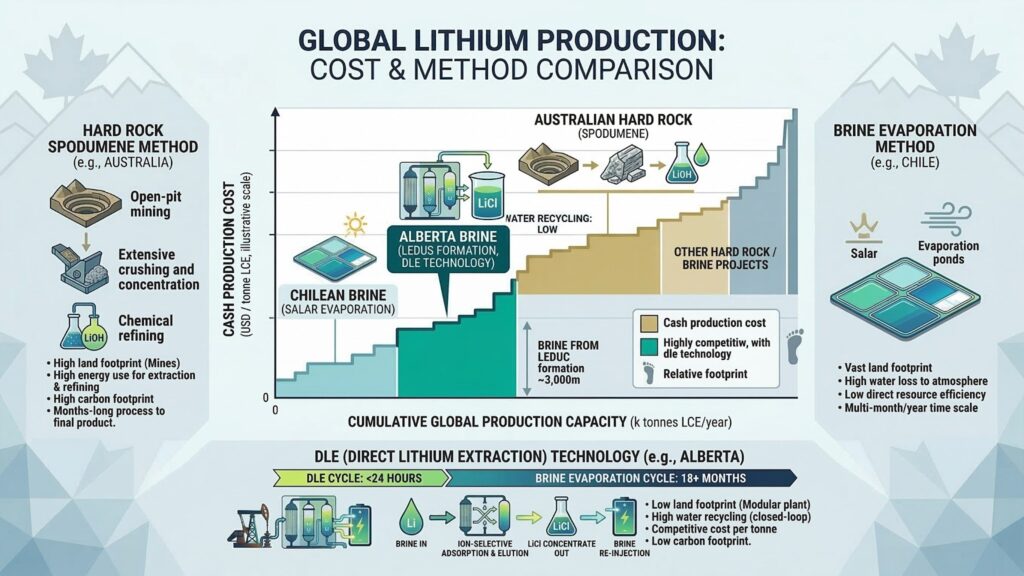

Recent assays, however, have revealed that these brines contain significant concentrations of lithium. While the concentrations (ranging from 50 to 100+ mg/L) are lower than those found in the salars of Chile or Argentina, the sheer volume of the reservoirs and the existing infrastructure make them economically viable.

The “Lithium Triangle” Concept

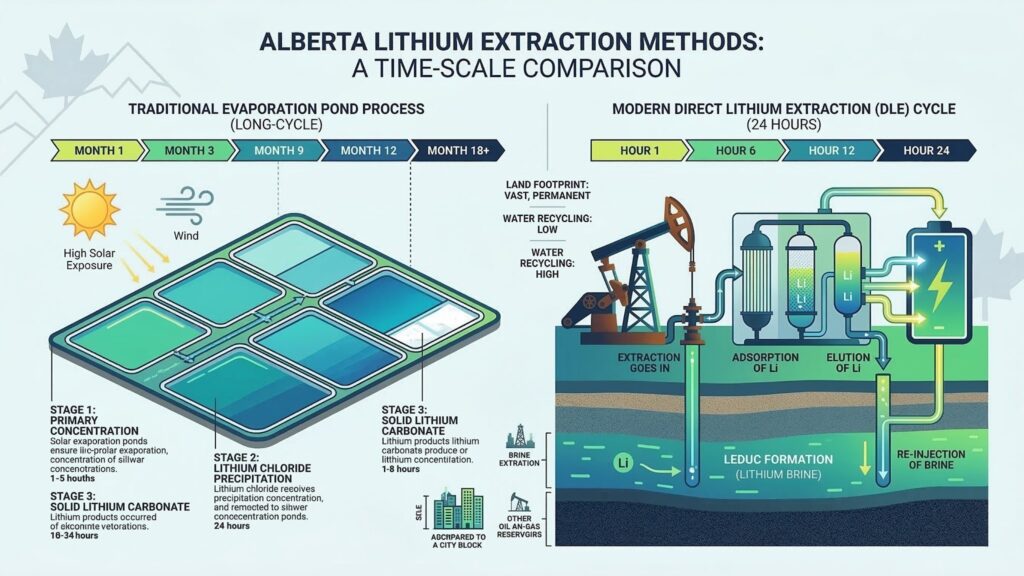

In South America, the “Lithium Triangle” refers to the high-altitude salt flats of Chile, Argentina, and Bolivia. Alberta is now being touted as the “Lithium Triangle of the North.” Unlike the South American model, which relies on massive evaporation ponds that take up to 18 months to produce lithium, Alberta’s industry is built on speed, technology, and a minimal surface footprint.

2. Direct Lithium Extraction (DLE): The Technical Core

The linchpin of Alberta’s lithium ambition is Direct Lithium Extraction (DLE). For technical engineers and investors, DLE represents the most significant shift in mineral processing in a generation.

How DLE Works

Unlike traditional evaporation, DLE uses chemical or physical processes to selectively remove lithium ions from the brine while leaving other minerals (like magnesium and calcium) behind. There are three primary types of DLE currently being tested in Alberta:

1.Adsorption: Using specialized sorbents that “catch” lithium ions as brine flows through a column.

2.Ion Exchange: A process where lithium ions in the brine are swapped with other ions (usually hydrogen or sodium) on a resin.

3.Solvent Extraction: Using organic liquids to pull lithium out of the aqueous brine solution.

The Engineering Advantage

The educational value of DLE lies in its efficiency. A DLE plant can process brine and produce lithium concentrate in hours rather than months. Furthermore, once the lithium is extracted, the “barren” brine is reinjected back into the reservoir. This maintains reservoir pressure and eliminates the need for massive tailings ponds or open-pit mines.

3. Leveraging the Oilfield DNA: Infrastructure Synergy

Alberta’s competitive advantage isn’t just the lithium in the water; it’s the $100 billion worth of infrastructure already sitting on top of it. This is where the term “Petro-lithium” originates.

Repurposing Brownfield Assets

A typical lithium startup in a greenfield location (like a hard-rock mine in Quebec or a salt flat in Africa) must spend hundreds of millions of dollars on roads, power lines, drilling rigs, and pipelines. In Alberta, these assets are already in place.

- Existing Wellbores: Thousands of suspended or active oil wells can be repurposed to pump brine.

- Geological Data: Alberta has arguably the best-mapped subsurface in the world. Companies don’t have to “guess” where the brine is; they have decades of well logs and seismic data provided by the Alberta Energy Regulator (AER).

- The Workforce: The same engineers, pipefitters, and chemists who manage complex oil refineries are perfectly suited to manage DLE facilities.

Case Study: E3 Lithium and the Clearwater Project

E3 Lithium, one of the province’s frontrunners, has secured a massive resource area in the Leduc formation. By utilizing DLE technology, they aim to produce battery-grade lithium hydroxide. Their strategy highlights the “Educational” aspect of the industry: they are not reinventing the wheel; they are changing the cargo.

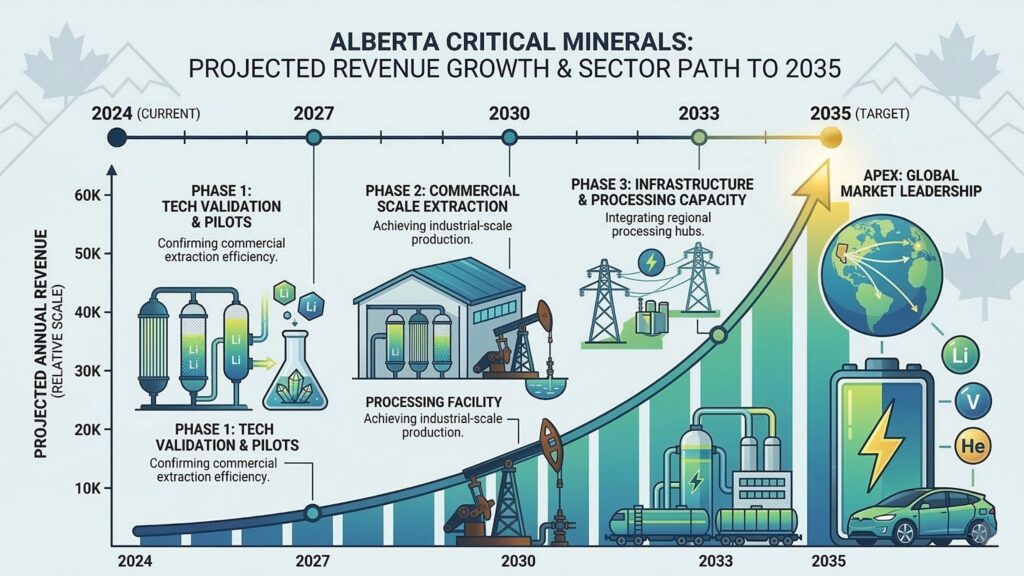

4. The Economic Multiplier: Jobs, GDP, and Diversification

From a senior economic analyst’s perspective, the lithium sector offers a rare opportunity for “counter-cyclical” growth. While oil prices are subject to OPEC+ decisions and global demand, the demand for lithium is tied to the structural shift toward electrification.

Job Creation for the Modern Era

The lithium industry is expected to create thousands of high-paying jobs in rural Alberta. These aren’t just “extraction” jobs; they are high-tech roles in:

- Chemical Engineering and Process Design.

- Software development for automated DLE plants.

- Environmental monitoring and hydrogeology.

Revenue Streams for the Province

In 2021, the Alberta government introduced the Mineral Resource Development Act, which established a clear regulatory framework for lithium. This allows the province to collect royalties, similar to oil and gas, which fund public services like healthcare and education.

5. The ESG Advantage: Greening the Battery Supply Chain

For investors, Environmental, Social, and Governance (ESG) metrics are no longer optional. The traditional lithium industry faces significant criticism:

- Hard Rock Mining (Australia/China): High carbon footprint due to crushing and roasting ore.

- Evaporation Ponds (South America): Massive water consumption in arid regions, often affecting local Indigenous communities.

Alberta’s Low-Carbon Lithium

Alberta’s petro-lithium model is inherently more sustainable.

1.Water Neutrality: Since the brine is reinjected, there is minimal impact on local freshwater tables.

2.Land Use: DLE plants have a footprint similar to a small gas plant, significantly smaller than an open-pit mine.

3.Carbon Sequestration Potential: Many DLE projects are exploring the use of Carbon Capture and Storage (CCS) to produce “Net-Zero Lithium,” a product that would command a premium price from automakers like Tesla or Ford.

6. Key Players and the Competitive Landscape

The Alberta lithium scene is currently a mix of agile startups and established energy giants.

The Startups

- E3 Lithium: Focused on the Leduc Aquifer, currently operating a field pilot plant.

- Volt Lithium: Targeting the Muskeg River Formation, they have reported high recovery rates using their proprietary DLE technology.

- Grounded Lithium: Focused on the Kindersley area (extending into Saskatchewan), emphasizing low-cost production.

- LithiumBank: Holding massive land positions in the Fox Creek and Peace River regions.

The Incumbents

We are seeing increasing interest from traditional energy companies. Imperial Oil, for instance, has partnered with E3 Lithium, providing both capital and technical expertise. This signal is crucial for investors: it shows that the “smart money” in the oil patch sees lithium as a viable hedge.

7. Challenges and Market Volatility

No economic analysis is complete without a sober look at the risks. The “Quiet Race” faces several hurdles:

1. Technology Scaling

While DLE works in a laboratory and at pilot scales, it has yet to be proven at a massive commercial scale in Alberta’s specific brine chemistry. The “Educational” challenge here is optimizing the sorbents to handle the high salinity and temperature of the Leduc brines without degrading.

2. Lithium Price Volatility

Lithium prices are notoriously volatile. The “white gold” rush of 2022 saw prices skyrocket, followed by a significant correction in 2023. Alberta producers must ensure their “All-in Sustaining Costs” (AISC) are low enough to survive price troughs.

3. Global Competition

Alberta is competing with the United States (Standard Lithium in Arkansas), Europe, and the established giants in the Lithium Triangle. Speed to market is essential.

8. Regulatory Framework: Bill 82 and Beyond

For business owners and investors, the regulatory environment is the “how-to” of entry. Alberta has moved aggressively to provide certainty.

- Bill 82 (Mineral Resource Development Act): This bill gave the Alberta Energy Regulator (AER) the authority to oversee lithium development. This is a massive win for the industry because the AER already has the systems in place to manage drilling permits and environmental assessments.

- Tenure Systems: Alberta has established a “Mineral Lease” system that allows companies to secure the rights to the lithium in the brine, separate from the oil and gas rights.

9. The Downstream Dream: A Battery Hub?

The ultimate goal for Alberta is not just to export raw lithium concentrate. The real economic prize lies in the downstream supply chain.

Value-Added Processing

Converting lithium concentrate into battery-grade lithium carbonate or hydroxide is a complex chemical process. Alberta, with its abundance of natural gas (for heat) and industrial chemicals, is an ideal location for these conversion facilities.

The Battery Belt

If Alberta can produce the lithium, and potentially other critical minerals like vanadium and nickel, the province could attract battery cell manufacturers. This would create a “closed-loop” economy, where minerals extracted in the Leduc formation are used in batteries manufactured in Edmonton or Calgary, powering EVs across North America.

10. Conclusion: The Strategic Imperative

Alberta’s foray into lithium is more than just a diversification play; it is a strategic imperative. As the world moves toward a low-carbon economy, the province’s survival depends on its ability to evolve.

The “Lithium Triangle of the North” offers a compelling narrative: a region that uses its 20th-century industrial might to solve 21st-century energy challenges. For the engineer, it is a playground of technical innovation. For the investor, it is a high-growth frontier. For the resident, it is a promise of continued prosperity.

The race is quiet, but the stakes couldn’t be higher. Alberta is no longer just an oil province; it is becoming an energy province in the broadest, most modern sense of the word.

Sources and References

1.Alberta Energy Regulator (AER): “Mineral Resource Development Act Guidelines and Brine-Hosted Mineral Data.”

2.Natural Resources Canada (NRCan): “The Canadian Critical Minerals Strategy – 2023 Update.”

3.E3 Lithium Investor Relations: “Clearwater Project Pre-Feasibility Study (PFS).”

4.University of Alberta, Department of Earth and Atmospheric Sciences: “Hydrogeological Mapping of the Leduc Formation.”

5.International Energy Agency (IEA): “The Role of Critical Minerals in Clean Energy Transitions.”

6.Government of Alberta: “Economic Recovery Plan: Focus on Critical Minerals.”