In the sun-drenched expanses of Southern Alberta, a quiet but profound transformation is underway. For over a century, the narrative of the province’s wealth was written in the black ink of crude oil. Today, however, a clear, odorless commodity is dictating the future of the regional economy. Water, once viewed as a communal certainty, has evolved into a high-stakes financial asset. As climate patterns shift and multi-year droughts become the “new normal,” the legal and economic frameworks governing water allocation are reshaping the very fabric of Alberta’s agribusiness sector.

From the boardrooms of Calgary to the pivot-irrigated fields of Lethbridge, the “Liquid Gold Rush” is on. This is not merely a story of environmental concern; it is a complex economic shift involving property rights, market-based transfers, and the urgent need for technological disruption in the food supply chain.

The following economic facts are based on current Alberta provincial data and market trends.

1. The Legal Bedrock: Understanding FITFIR and the Water Act

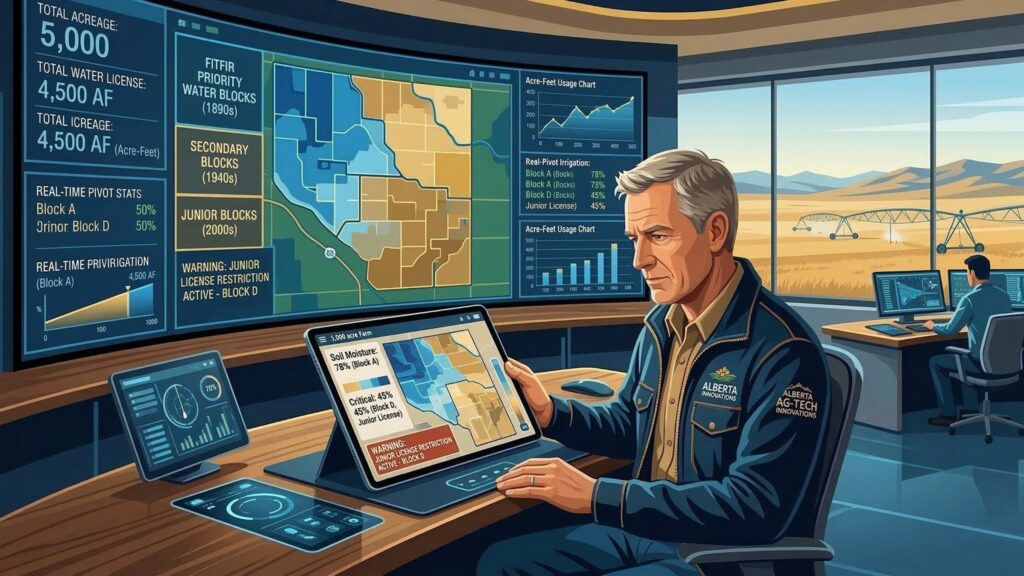

To understand the economics of water in Alberta, one must first understand the legal doctrine of “First-in-Time, First-in-Right” (FITFIR). Established during the late 19th century, this system governs how water is allocated during times of scarcity.

The Seniority System

Under the Alberta Water Act, licenses are granted with a priority number based on the date the application was first made. In a drought year, “senior” license holders (often irrigation districts or long-established municipalities) are entitled to their full allocation before “junior” holders (newer industrial projects or recent agricultural expansions) receive a single drop.

- Senior Licenses: Typically dated pre-1950. These are the “blue chips” of the water world.

- Junior Licenses: Post-1990. These carry significant operational risk during low-flow years.

The Moratorium on New Licenses

In the South Saskatchewan River Basin (SSRB), the provincial government stopped issuing new water licenses in 2006. This created a closed market. If a new processing plant or a high-intensity farm wants to operate, they cannot simply apply for water; they must buy or lease the rights from an existing holder.

2. The Economic Valuation of Water Rights

As the supply of new licenses remains frozen and demand increases due to population growth and industrial expansion, the market value of water rights has skyrocketed.

The Rising Cost per Acre-Foot

An “acre-foot” (the volume of water required to cover one acre of land to a depth of one foot) has become a standardized unit of trade. While prices vary based on the reliability of the source, recent market observations indicate:

- Historical Prices (Early 2000s): $500 – $1,000 per acre-foot.

- Current Market Estimates: $5,000 – $15,000+ per acre-foot depending on seniority and location.

Water as an Intangible Asset

For many Southern Alberta farms, the water license is now more valuable than the deed to the land itself. Financial institutions are increasingly scrutinizing water seniority when assessing agricultural loans. A farm with 1,000 acres but only junior water rights is viewed as a high-risk investment compared to a smaller plot with senior, “bulletproof” water security.

3. Drought as an Economic Chokepoint

The 2023 and 2024 seasons have highlighted the fragility of the system. With the mountain snowpack—the “water tower” of the prairies—hitting record lows, the economic ripple effects are being felt across the province.

The 2024 Water Sharing Agreements

In an unprecedented move, the Alberta government facilitated the largest water-sharing agreement in provincial history in early 2024. Major users, including the City of Calgary, the City of Lethbridge, and several large irrigation districts, agreed to voluntarily reduce water usage if conditions worsened.

- Economic Impact: These agreements prevent the “nuclear option” of a senior holder cutting off a junior holder entirely, which would cause catastrophic industrial shutdowns. However, they also necessitate a reduction in crop yields and industrial throughput.

The “Dryland” vs. “Irrigated” Divide

The economic disparity between dryland farming (relying on rainfall) and irrigated farming is widening. In drought years, dryland yields can drop by 60-80%, while irrigated land remains productive, albeit at a higher cost. This is driving a massive consolidation of land toward those who can afford the infrastructure and the water rights to sustain it.

4. The Great Pivot: Adapting the Agribusiness Model

Faced with the reality of water scarcity, Alberta’s farmers are not simply waiting for rain; they are pivoting their business models to maximize “dollars per drop.”

From Thirsty to Thrifty: Crop Selection

Traditionally, Southern Alberta was a powerhouse for forage crops like alfalfa, which are notoriously water-intensive. We are now seeing a shift toward:

1.Pulse Crops: Lentils and chickpeas require significantly less water than traditional cereals or forages.

2.Winter Wheat: By planting in the fall, farmers capitalize on early spring moisture, often harvesting before the peak heat and drought of July and August.

3.Specialty Seeds: Hybrid canola and specialized sugar beet varieties engineered for drought tolerance.

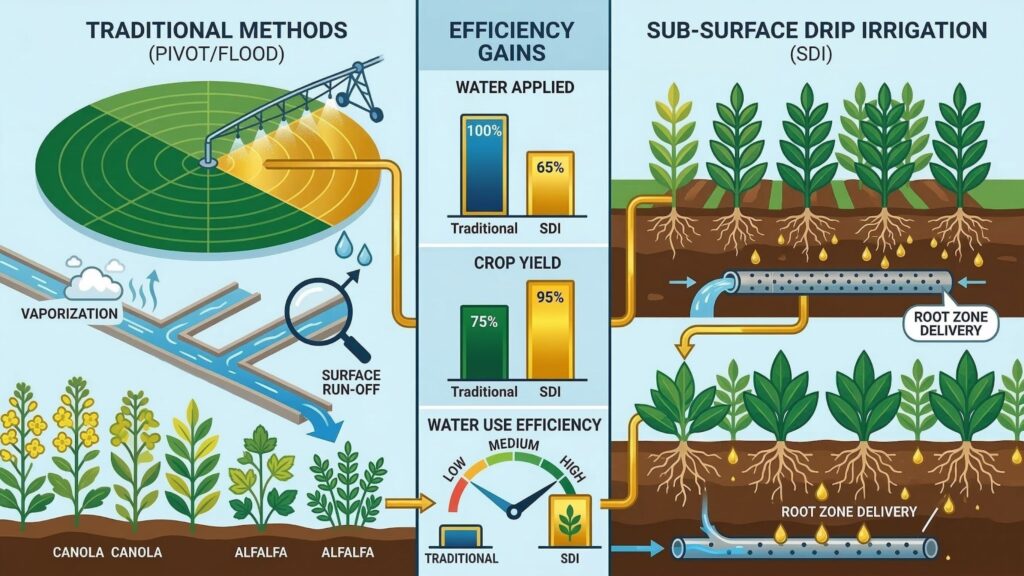

Precision Agriculture and Variable Rate Irrigation (VRI)

The “how-to” of modern Alberta farming involves intense technological integration.

- VRI Systems: These use GPS and soil moisture sensors to apply specific amounts of water to specific parts of a field, avoiding overlap and reducing waste.

- Sub-Surface Drip Irrigation (SDI): While expensive to install, SDI delivers water directly to the root zone, eliminating evaporation losses—a critical factor when temperatures exceed 30°C.

5. Infrastructure: The $933 Million Bet

The Alberta government, in partnership with the Canada Infrastructure Bank and various irrigation districts, has embarked on a nearly $1 billion investment in irrigation infrastructure. This is the largest expansion of its kind in modern Alberta history.

Modernizing the “Veins” of the Province

The goal is not necessarily to use more water, but to use the existing allocation more efficiently.

- Canal Lining and Piping: Replacing open-earth canals with PVC piping eliminates seepage and evaporation. This “saved” water can then be used to expand the total number of irrigated acres without increasing the total withdrawal from the river system.

- Off-Stream Storage: Building new reservoirs to capture peak spring runoff (meltwater) so it can be released slowly during the dry summer months.

6. Economic Ripple Effects on the Food Supply Chain

Alberta is home to a massive food processing cluster, particularly in the “Canada’s Premier Food Corridor” (the region between Lethbridge and Taber). Companies like McCain Foods, Cavendish Farms, and Rogers Sugar rely on a steady, predictable supply of raw agricultural products.

The Risk to Processing Investments

Processing plants require millions of liters of water daily for sanitation and production. If water rights become too volatile or expensive:

- Capital Flight: New processing facilities may look to jurisdictions with more stable water outlooks.

- Supply Chain Inflation: As farmers pay more for water, the cost of raw potatoes, sugar beets, and wheat rises, eventually hitting the consumer at the grocery store.

The Opportunity for “Water-Neutral” Tech

Conversely, this scarcity is breeding a new sub-sector of the economy: water-tech engineering. Alberta is becoming a testing ground for industrial water recycling and closed-loop systems, creating high-paying jobs for technical engineers and environmental consultants.

7. The Investor Perspective: Is Water the New Asset Class?

For investors and business owners, the “Liquid Gold Rush” presents a unique set of risks and rewards.

Risks

- Regulatory Change: There is ongoing political pressure to reform the FITFIR system to prioritize “social good” or “environmental flows” over historical rights. Any change to the Water Act could strip value from existing licenses overnight.

- Climate Volatility: If snowpacks continue to decline, even a senior license may not guarantee water if the river literally runs dry.

Opportunities

- Water Aggregators: Companies that buy fragmented water rights, consolidate them, and lease them back to high-value users.

- Ag-Tech Stocks: Investing in companies providing the sensors, drones, and software that power precision irrigation.

Conclusion: Resilience Through Value

The era of “cheap and easy” water in Alberta is over. As water rights continue to reshape the agribusiness landscape, the province is moving toward a more sophisticated, market-driven approach to resource management. While the challenges of drought are significant, they are also driving an unprecedented wave of innovation.

For the potential resident or investor, Alberta’s agribusiness sector remains a powerhouse, but its future success is now inextricably linked to the management of its most precious liquid asset. Those who understand the nuances of the Water Act and the mechanics of irrigation efficiency will be the ones to thrive in this new economic reality.

Sources and References

1.Alberta Environment and Protected Areas: Current Water License Statistics and SSRB Allocation Reports.

2.Alberta Agriculture and Irrigation: The 2023-24 Irrigation Expansion Project Overview.

3.University of Lethbridge, Department of Economics: Studies on the Market Value of Water Transfers in Southern Alberta.

4.The Water Act (R.S.A. 2000, c. W-3): Provincial Legislation on FITFIR and License Transfers.

5.Canada Infrastructure Bank: Project Finance Data for Alberta Irrigation Districts.

6.Alberta Water Portal Society: Historical Snowpack and Reservoir Level Comparisons (1970-2024).